As unusual as it could sound, incomes monetary freedom is lots simpler for sure individuals than claiming that freedom as soon as they’ve earned it. And if the next assertion rings true to you, you might be affected by this similar hardship:

“I think I’m close to having enough money to jump into early retirement, but not quite.

So I’m just working one more year and starting one more side hustle and buckling down extra hard to be more certain.”

It sounds rational, proper? In any case, you possibly can by no means be too cautious, because the saying goes.

However the issue is that these individuals maintain repeating the mantra no matter how a lot cash they’ve, and no matter their precise dwelling bills. Regardless of how vivid their monetary image is, they all the time discover a technique to undervalue their financial savings and overestimate their future bills, simply in case of the surprising.

And by tilting the stability ever additional within the path of “safety”, they overlook about what ought to be on the opposite facet of the size, which is “making the most of your finite time on this lovely planet.”

This occurs far more than you may assume. Each week, it’s in my e mail inbox and my in-person conversations with individuals I meet. This concern is even prevalent amongst a few of my real-life associates, so let’s have a look at a few thinly disguised examples from that group to see a few of the signs (and a attainable treatment for) this famed affliction of One Extra 12 months Syndrome.

Alina’s Anemic Withdrawal Fee

Alina is a currently-single physician in a annoying however effectively paid space of follow, age 50 with one grown little one. She has about $2 million in investments, and at present spends about $50,000 per yr, a stage which incorporates just about all the things that’s essential to her.

Based on The 4% Rule, Alina’s nest egg will present a reasonably dependable earnings of roughly $80,000 per yr for the remainder of her life. Or to place it one other manner, her deliberate spending of $50k is barely a 2.5% withdrawal charge from that 2 million. Since 4% within reason secure, 2.5% is a preposterously secure withdrawal charge.

However wait! There’s extra. Within the curiosity of being conservative, Alina has intentionally ignored a number of different key items of her personal monetary future:

- All future social safety earnings (over $2000 per 30 days for the final 2-3 many years of your life)

- A extremely possible inheritance from her mother and father who, whereas clever and vibrant and nonetheless doing nice, are of their early 80s.

- And he or she’s additionally assuming that she’s going to by no means couple up with one other companion sometime and share family bills, even though she’s a horny and sociable particular person with many choices on this division.

Her response to this sense of additional warning? Simply crank it out for one more yr or three within the furnace of the working room, and maintain off on any luxuries to avoid wasting up one other few hundred thousand, simply in case.

Dave’s Deceptively Shiny Future

My different buddy Dave is ten years youthful, with a decrease earnings however equally scrappy and really entrepreneurial. He has been a star performer in a really underpaid full-time job for over fifteen years. His complete annual spending – together with a mortgage on a $430,000 home right here in Longmont – is barely about $45,000 per yr.

Though Dave lives in high-cost Colorado, he has fastidiously accrued eight rental flats again in his hometown (a midsized metropolis in Ohio), which very conservatively ship $2800 per 30 days of internet cashflow, whereas additionally growing his wealth by an extra $3000 each month by way of principal payoff and appreciation.

He additionally has a few facet jobs, serving to numerous members of our native HQ Coworking house with their companies, which usher in an extra $1000 per 30 days.

After which the kicker: Over the previous seven months, Dave and I teamed as much as renovate the principle flooring of that considerably expensive new home into a really high-end Airbnb rental. We just lately pressed the button to make this place go reside, and it turned a right away success with nearly no emptiness, now bringing in one other $5000 per 30 days (!?), whereas nonetheless leaving him together with his completed walkout lower-level condo as a spot to reside.

So, Dave resides in his personal basement accumulating $5000 each month, whereas spending solely $2000 on the mortgage. In different phrases, he’s dwelling free of charge and getting paid an extra $3000 for the chore of proudly owning this home, a trick formally referred to as the “Mustachian Inversion”

Should you add all this up, he has a complete enterprise earnings of $8800 per 30 days ($105,600 per yr!), which completely dwarfs his $45,000 spending even with out considering the wage from that crappy full-time job which he has been desirous to give up for thus lengthy.

While you add within the further $3000 per 30 days of mortgage principal payoff and appreciation of the leases, my buddy’s facet hustles are netting him $140,000 yearly. And his financial institution accounts mirror this: there are sizable money reserves and upkeep and contingency funds for each rental unit, plus a well-funded private 401k plan and each different little bit of accountable monetary preparation you possibly can think about.

You could be barely jealous of Dave as a result of he’s all set to chill and benefit from the proceeds of all this difficult work for all times. He may reduce his earnings in half and his wealth would nonetheless enhance quickly ceaselessly.

However keep in mind, on prime of all this he nonetheless has that full time job which is demanding about 10 hours of his time each day, with a number of hours of Zoom conferences packed in all through, eliminating the potential for slacking.

Dave is a good sport and places on a courageous face, however all of us within the native associates group can inform that he’s practically buckling beneath the stress of this shitty, annoying job, particularly mixed together with his overflowing salad bowl of facet hustles.

“Dave, you stubborn dumbass, you need to quit that job yesterday”,

is the loving message we’ve got been attempting to get into his head.

“Yeah, I know”, he says, “But I’m just holding on for one more year, just to pad the accounts a bit further. What if the Airbnb slows down? What if my rental houses experience some vacancy? What if I want to help my nephew with college ten years down the line?”

Alina and Dave are each leaning upon the previous rule of “You can never be too safe”, and many individuals agree with that assertion, as a result of how may you argue with such plain folksy knowledge?

However this rule is wrong. It’s certainly attainable to be “too safe”, as a result of security comes at a excessive price – and the value is your personal life.

If Dave enjoys good well being and lives to age 90, he nonetheless solely has about 600 months left to reside, or an much more treasured 240 months of “youth” earlier than hitting age 60. And Alina’s remaining 120 months of youth are much more pricey.

With each of their monetary conditions already so comfortable, why oh why are my pricey associates buying and selling away this time for jobs they don’t take pleasure in, simply to get that final shred of pointless security?

Why are they letting these jobs compromise their friendships and relationships, price them sleep, miss out on tenting journeys and worldwide adventures and simply plain lazy Tuesday brunches with the individuals they love probably the most? (most of whom are already retired and at present having brunch with out them?)

The actual reply in fact is just not cash, it’s concern.

However for those who dig deeper, their concern remains to be about “running out of money”, though it’s virtually mathematically not possible at this level.

To coach away this concern in myself and others, I prefer to conduct a thought experiment. And that’s to power your self by way of the numbers (utilizing a spreadsheet) of those two issues.

- Should you give up your job proper now, what would a great, typical, and improbably unhealthy situation appear like on your monetary future?

- Then within the case of the “bad” situation, write down, step-by-step, what it will actually imply so that you can run out of cash.

This could be a loopy thought experiment, however in lots of circumstances it’s going to additionally reveal simply how a lot of a ridiculously lucky fortress you may have constructed for your self.

As a result of in contrast to you, most individuals within the US actually are virtually out of cash. They’ve nearly no retirement financial savings, month-to-month spending that meets or exceeds their earnings, and an array of automobile loans, scholar loans, and bank card debt that grows yearly. A full ten % of households have a damaging internet value, and even the median internet value is beneath $100,000 which means half of us have solely a 1-2 yr cushion between ourselves and being useless broke.

If the common particular person quits their job, any shreds of internet value can be depleted virtually instantly. At this level, the owner and the gathering companies come calling, and they might actually find yourself with no meals or shelter past what is out there by way of welfare applications. It’s a tough place to be, however this class contains tens of tens of millions of individuals within the US.

However for many Mustachians contemplating early retirement, the scenario is totally totally different. And to show this level, let’s attempt to get Alina to go bankrupt.

(observe: I made all the spreadsheets and graphs beneath in “real” (inflation-adjusted) {dollars} so that they make extra sense from our perspective of as we speak. In actuality, all of the numbers (each spending and investments/earnings) will get greater over time relying on the speed of inflation, however the internet impact is similar)

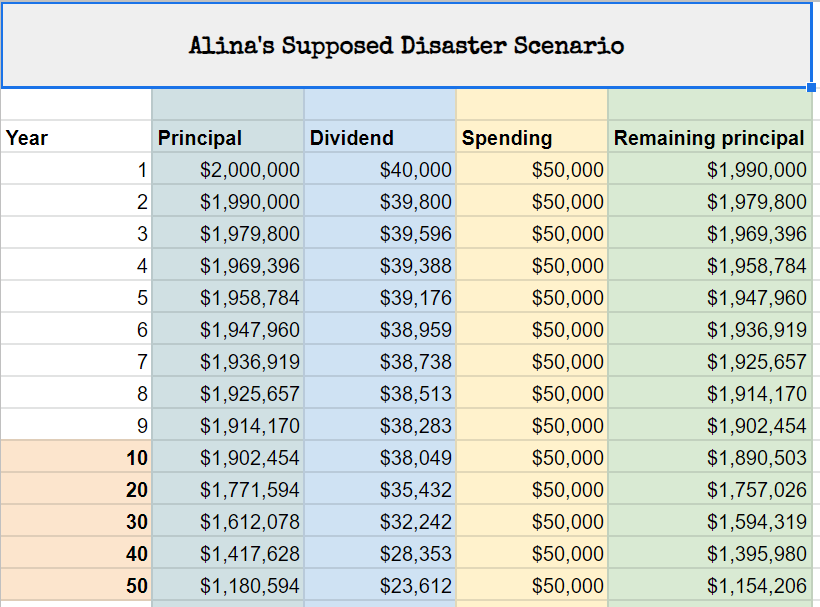

Alina: The Worst Case Situation

As a substitute of “one more year”, she quits her job now.

Though the inventory market tends to develop together with the financial system, let’s assume we enter a by no means ending interval of stagnation the place shares barely even match inflation, and she or he decides to reside solely off of the dividends of her $2 million portfolio, that are a paltry 2% in the intervening time, or $40,000 per yr.

However regardless of her conservative funding administration, she insists on protecting her spending on the full $50k. She by no means rents out an condo in her home, by no means finds any pastimes that generate any earnings, by no means switches from Entire Meals to Costco, retains up the worldwide journey, and all the time retains a new-ish automobile within the driveway even though she has no extra commute.

The US Social Safety program someway will get canceled even though our getting old inhabitants carries the majority of the voting energy and would by no means vote away its personal retirement earnings, and her mother and pa determine to donate all their remaining wealth to charity relatively than leaving it to Alina and her sister.

Within the occasion of this ridiculously contrived instance, she would find yourself drawing down $10,000 per yr from her financial savings, which suggests her wealth would drain all the way down to, uh-oh, 1.99 million after the primary yr. And the pattern would proceed like this:

Uh-oh. So the worst issues have occurred in lots of areas of her financial life, and Alina lives out the subsequent 40 years of her life and dies with solely $1,395,000 within the account. What a harrowing shut name!

However what if issues turned out worse than the worst? Regardless of our greatest efforts to make her go bankrupt, she nonetheless died a millionaire. So we have to get slightly extra Mad Max in our situation:

Alina: Fury Street

The US decides to cripple its personal financial system ceaselessly so there isn’t any extra innovation, no productiveness, and all dividends are halted and but our 330 million residents all determine to go together with it.

Amid the chaos and the dune buggy machine gun battles which rage day and night time on the street, her wealth drains by $100,000 yearly and she or he is all the way down to a single million by age 60. However she retains up the spending and refuses to make any modifications. She’s broke by age 70 however simply sticks to her favourite actions that are rewarding and interesting however by no means produce a penny of earnings.

Her mortgage checks begin to bounce. The financial institution ultimately enters foreclosures however she stays glued to that home. After one other yr, the foreclosures is full and the sheriff arrives to tug her wiry 71-year-old body out of the home, kicking all the way in which.

Alina is eligible for social applications, however rejects all of them. She has an enormous community of associates, however doesn’t settle for any of their affords for assist or employment.

She checks into a pleasant all-suites lodge and begins paying all her payments with bank cards, maxing all of them out together with some money advances to maintain the cash flowing. With the standard tips of stability transfers and delayed-repayment plans, she retains the celebration going for 2 extra years, till all of the bank cards have been canceled and despatched off to collections.

At age 73, Alina is lastly out of cash. She can’t purchase meals or shelter and she or he has lastly arrived at a actuality that homeless individuals at present expertise each day proper now. However we needed to make up a completely ridiculous and admittedly not possible story to get her there.

I’ll spare you the lengthy story of Dave’s decline, but it surely’s equally not possible.

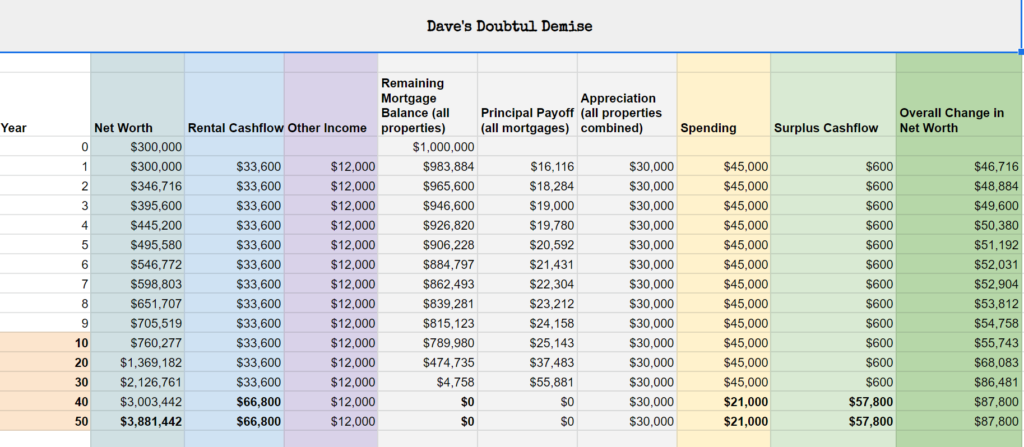

Dave’s Uncertain Demise

If he give up his job as we speak, stopped airbnbing his home and simply loved the entire thing and by no means even rented out the decrease stage, forfeited his six-figure 401k account and social safety and all the things else besides the rental properties and the $1000 from native gigs, this is able to occur:

What the heck!?

We threw Dave into the worst of conditions, one thing far past simply quitting his crappy day job and arguably not possible. But not solely does his cashflow proceed to extend, however his internet value skyrockets by about $50,000 per yr, ending up at virtually $4 million {dollars} (inflation-adjusted too) by the point he kicks the bucket at 90 years previous.

In actuality, that purple “other income” column is more likely to be triple what the spreadsheet says, his 401(okay) account will certainly live on and develop, and lots of different good issues will occur.

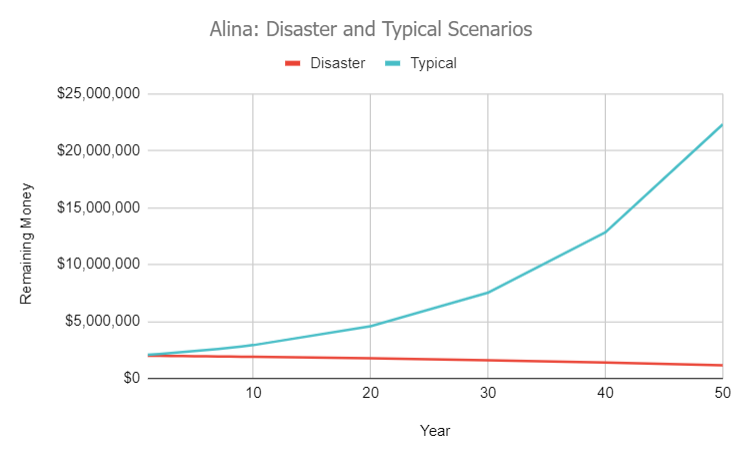

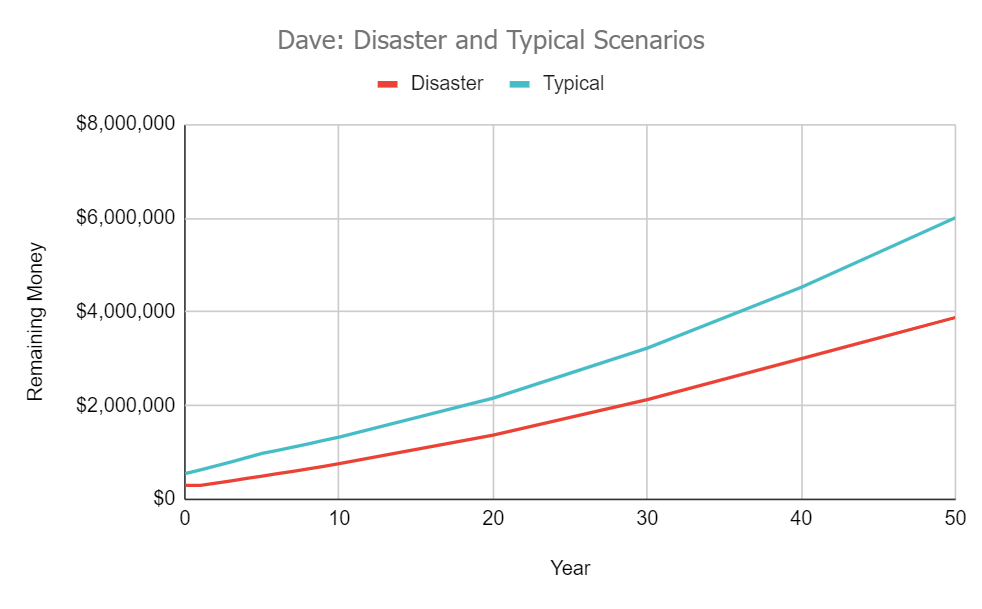

Extra Real looking Projections for Each Of My Associates

Should you’re a pessimist, you might have checked out all of these numbers above and stated, “Hmm yeah they made it, but it was a little close”. However keep in mind, these have been worst case eventualities. It’s silly to plan all the things in your life across the worst case situation, as a result of it’s going to typically end in you having the minimal attainable quantity of enjoyable.

So as an alternative, you want to not less than embody a conservative estimate of what’s probably to occur. And I’ve executed so for each Alina an Dave, creating these graphs of the outcomes

So, each of those associates cannot solely give up working, they’ll additionally begin forking out extra money on no matter they need. Congratulations to each of you!

Each of them, and extra importantly a big proportion of MMM readers, presumably together with YOU, are past the purpose the place they might ever run out of cash even when they give up their jobs as we speak.

And they should see this excellent fact for what it’s, in order that they’ll confidently act on it, in order that they’ll cease gifting away treasured months of their lives away to their employers, to amass nonetheless extra chunks of straightforward cash, so as to add to a pile that they are going to by no means, ever, ever want.

After which they’ll begin experiencing precise actuality of early retirement, which is as follows:

- Your spending finally ends up slightly bit decrease than you anticipated, regardless of your greatest efforts to splurge on your self and be beneficiant to others.

- Your investments do maintain going up over the long term, exceeding these conservative forecasts you made.

- You do find yourself making bits of cash right here and there (in Dave’s case shit-tons of cash), though you completely don’t want it.

- Because the many years cross and you compromise into this sample, you understand that cash is just not one among your worries. Life as a Human Being nonetheless presents loads of challenges, however holy shit, thank goodness you give up working whenever you did as a result of it was utterly pointless. Wanting again, you in all probability ought to have executed it a number of years earlier.

If any of this sounds acquainted, congratulations – you’ll by no means run out of cash which suggests you want to cease letting it rule your life.

Stop your job.

Severely.

Sheesh. What are you ready for?!

Epilogue: Mr Cash Mustache Chills out for a Splurge too:

Writing this text jogged my memory that I can also nonetheless be a sufferer of excessively frugal habits. Certain, my home is gorgeous and I’ve nice meals, vehicles, instruments, bikes and all the things else. However in relation to journey, I begin enjoying foolish video games with myself.

For instance, my boy and I are heading to Canada later this month to go to the household. And in opposition to all logic, I seen the Nagging Voices of Cheapness beginning to chatter in my head.

“These plane tickets were only $210 each – can I really justify paying an extra $80 for a bigger seat at the front of the plane? And sheesh, how can I get around the $150 roundtrip Uber ride (or $150 roundtrip driving+parking) to the airport, that’s ALMOST AS MUCH AS THE PLANE TICKET! Should we spend an extra 3 hours roundtrip to save $100 by taking the bus?” After which what about our transportation as soon as we’re in Canada? Bus? Automotive rental? Prepare tickets? How does the $7.00 per gallon gasoline issue into this on condition that we have to journey over 800 miles throughout our time there?

Blah blah blah. The proper reply is “Shut up, Mustache! You should do whatever you think is most fun and least stressful, without thinking about the money.”

For me, this implies driving my good electrical automobile on the speedy toll highway to the costly Denver Airport car parking zone so we are able to stroll proper into the terminal with no shuttle. It additionally means sitting in a great airplane seat, after which taking the least annoying and most enjoyable type of transportation as soon as I get there.

Why? As a result of the distinction between the most affordable and most annoying journey, and the most costly one on this case, is barely about one thousand {dollars}.

Even when I did this each single yr for the remainder of my life, I’d blow $50,000 on luxurious journeys to go to my household (and I may drive my Mother to her one hundred and twenty fifth birthday in fashion!)

And based mostly by myself worst-case spreadsheet, I’m by no means going to get up and assume,

“Damn, if I just had one thousand more dollars, or even fifty thousand dollars more in this net worth column, I’d be a happier person”

So I get to chill out, and luxuriate in my journey, and guess what I even did this:

So I’ll see you in retirement, and perhaps even in Canada later this month!

Additional Homework for Spreadsheet Lovers:

I’ve shared a replica of the Google Sheets spreadsheet I made for these examples and graphs right here. It is best to be capable to “file->make a copy” to get an editable model to fiddle with. Mine are fairly primary and pass over some particulars to be able to keep away from getting any extra sophisticated than they already are, however be happy so as to add extra for those who like,

Within the Feedback:

Are you too fearful, or too optimistic, or someplace in between? In case you have already give up your job, how did you get the boldness? Should you’re nonetheless caught in One Extra 12 months Limbo, what wouldn’t it take to get you out of it?

#Youll #Run #Cash

Leave a Reply